121 North Compass Way Dania Beach, Florida, 33004 (USA)

121 North Compass Way Dania Beach, Florida, 33004 (USA)

- 121 North Compass Way Dania Beach, Florida, 33004 (USA)

Loading content...

Contact us for more information or to schedule a meeting with our experts

Introduction:

Today, we’re diving deep into the fascinating world of blockchain technology – a revolutionary concept that has transformed industries and continues to shape the future of digital transactions and data management.

In this article, we’ll take you on a journey through the pros and cons of blockchain, shedding light on its potential applications in the years to come.

Understanding Blockchain: The Basics:

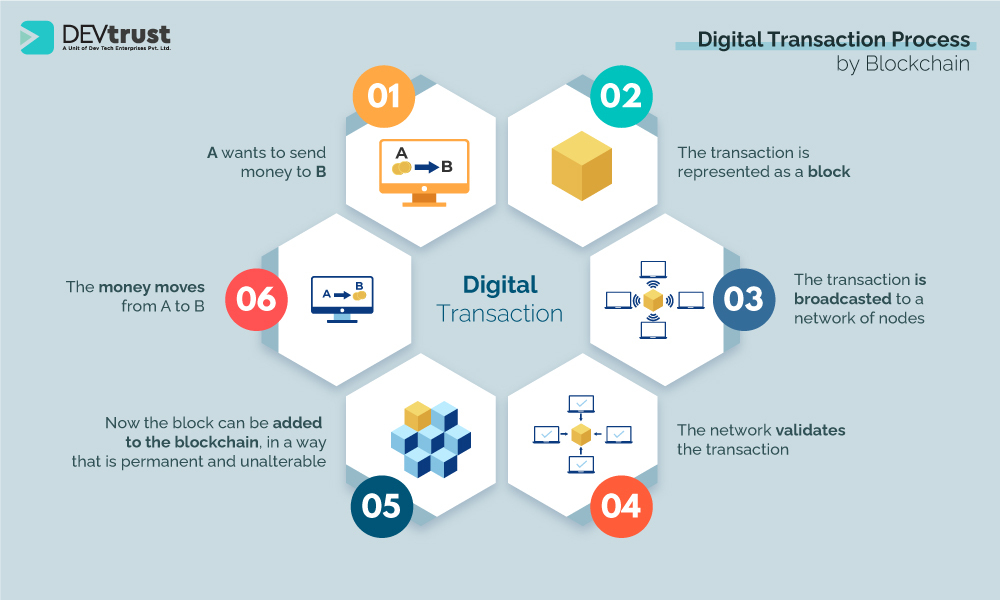

Blockchain, often dubbed as the “distributed ledger technology,” is a decentralized and tamper-proof system that records transactions across multiple computers. Instead of relying on a central authority, like a bank or government, blockchain transactions are validated by a network of participants through consensus mechanisms. This technology gained its initial recognition as the backbone of cryptocurrencies, particularly Bitcoin. However, its capabilities extend far beyond digital currencies.

Blockchain, often dubbed as the “distributed ledger technology,” is a decentralized and tamper-proof system that records transactions across multiple computers. Instead of relying on a central authority, like a bank or government, blockchain transactions are validated by a network of participants through consensus mechanisms. This technology gained its initial recognition as the backbone of cryptocurrencies, particularly Bitcoin. However, its capabilities extend far beyond digital currencies.

The Pros of Blockchain Technology:

Decentralization and Security: Blockchain’s decentralized nature eliminates the need for intermediaries, reducing the risk of fraud and unauthorized access. Each transaction is cryptographically linked to the previous one, creating an immutable record that’s incredibly difficult to alter.

Transparency and Trust: Public blockchains offer unparalleled transparency. Participants can access a complete, real-time history of transactions, enhancing trust among users.

Efficiency and Cost Savings: Traditional financial processes often involve several intermediaries and extensive paperwork. Blockchain streamlines these processes, reducing the time and costs associated with middlemen.

Smart Contracts: Blockchain enables the creation of self-executing contracts, known as smart contracts. These contracts automatically execute predefined actions when specific conditions are met, further reducing the need for intermediaries.

The Cons of Blockchain Technology:

Scalability: While blockchain ensures security, its decentralized nature can hinder scalability. As the network grows, transaction speed can decrease, leading to potential bottlenecks.

Energy Consumption: Many blockchain networks, particularly proof-of-work-based ones, require significant computational power, contributing to high energy consumption and environmental concerns.

Lack of Regulation: The absence of clear regulations can lead to uncertainty in legal matters, inhibiting wider adoption in some industries.

Irreversible Transactions: The immutability that makes blockchain secure can also be a drawback. Mistaken or fraudulent transactions are almost impossible to reverse, making user error a significant concern.

Future Possibilities:

The future of blockchain technology is incredibly promising. As scalability and energy efficiency concerns are addressed, we can expect to see widespread adoption across various sectors. From supply chain management and healthcare records to digital identity verification and beyond, blockchain has the potential to revolutionize how data is stored, verified, and exchanged.

Imagine a world where cross-border payments are settled in minutes, where medical histories are securely accessible to healthcare providers, and where every step of a product’s journey from manufacturer to consumer is transparently tracked. These possibilities are becoming more attainable as blockchain technology continues to evolve.

Imagine a world where cross-border payments are settled in minutes, where medical histories are securely accessible to healthcare providers, and where every step of a product’s journey from manufacturer to consumer is transparently tracked. These possibilities are becoming more attainable as blockchain technology continues to evolve.

Conclusion:

In conclusion, blockchain technology is poised to reshape the way we conduct transactions and manage data. Its inherent security, transparency, and potential for automation make it a compelling solution for a wide range of industries. While challenges exist, ongoing innovation and investment indicate a promising road ahead.

Keep an eye on www.devtrust.biz for more updates on blockchain technology and its exciting future applications!

Sources:

https://www.investopedia.com/terms/b/blockchain.asp

https://www.blockchain.com/what-is-blockchain

https://cointelegraph.com/learn/what-is-a-cryptocurrency-a-beginners-guide-to-digital-money

https://hbr.org/2017/01/the-truth-about-blockchain

https://www.technologyreview.com/2021/02/01/1017011/limitation-and-potential-of-blockchain-technology/

https://www.thebalance.com/negative-aspects-of-blockchain-technology-4172340

https://www.cbinsights.com/research/